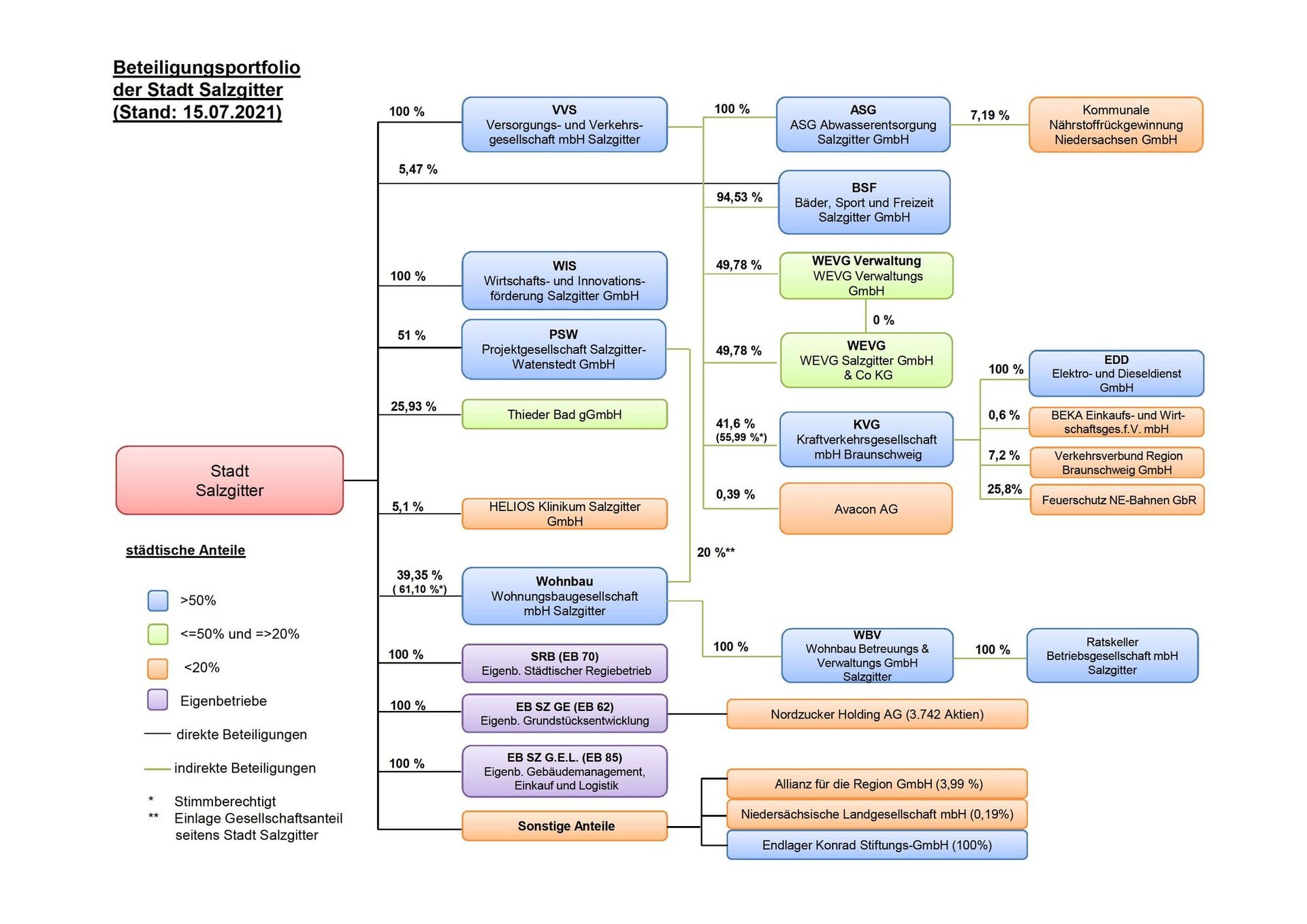

With the preparation of the consolidated financial statements, municipalities in Lower Saxony have been obliged since 2012 to combine their own annual financial statements with those of their subsidiaries in order to reflect the actual extent of their economic activity as municipal groups.

The consolidated financial statements are annual financial statements for the City of Salzgitter Group, which is considered an economic unit and provides an aggregated overview of assets and liabilities, increases and decreases in value and inflows and outflows of cash and cash equivalents. This information is intended to provide a more comprehensive insight into the financial impact of municipal and political action, particularly in terms of intergenerational equity.

However, there are a number of hurdles to overcome when preparing the consolidated financial statements. For example, the annual financial statements of the City of Salzgitter and those of its subsidiaries are not prepared in accordance with the same accounting standards due to the legal basis, meaning that a certain amount of translation work has to be carried out for the consolidation, which can be difficult, particularly in the case of matters dating back a long way. To date, the City Council of Salzgitter has only been able to unanimously approve the consolidated financial statements for 2012 on December 21, 2015. However, the preparation of the subsequent consolidated financial statements failed despite intensive efforts.

The city of Salzgitter was not alone in these problems, so that the state of Lower Saxony, in coordination with the municipal umbrella organizations, initiated an amendment to the Lower Saxony Municipal Constitution Act (NKomVG), which made it possible to dispense with the consolidated financial statements for the years 2012 to 2020. By resolution of the Council on December 21, 2021, the preparation of the financial statements of the City of Salzgitter Group for the years 2013 to 2020 was consequently waived in accordance with Section 179 (1) No. 1 NKomVG. The municipal supervisory authority had previously recommended this in the approval of the 2021/2022 double budget.

This now enables the renewed first-time consolidation for 2021, which means that the Council can finally be presented with consolidated financial statements that are up-to-date for the year and therefore actually relevant for management purposes from 2022.